Can I Pay Student Loans With Credit Card? The Ultimate 2026 Guide

Discover the loopholes, uncover the hidden fees, and learn exactly how to protect your credit score while managing education debt.

Millions of graduates face a massive financial burden every month. Consequently, many borrowers look for creative strategies to manage their debt efficiently. A very common question surfaces constantly: can I pay student loans with credit card? The answer involves complex banking rules, hidden transaction fees, and significant risks to your credit profile. Therefore, you must understand the exact mechanics before you attempt this financial maneuver.

Furthermore, taking on high-interest consumer debt to pay off education loans can quickly damage your long-term wealth. In this comprehensive guide, we reveal the truth behind direct payments. We also explore the third-party workarounds and analyze whether credit card rewards actually justify the processing fees.

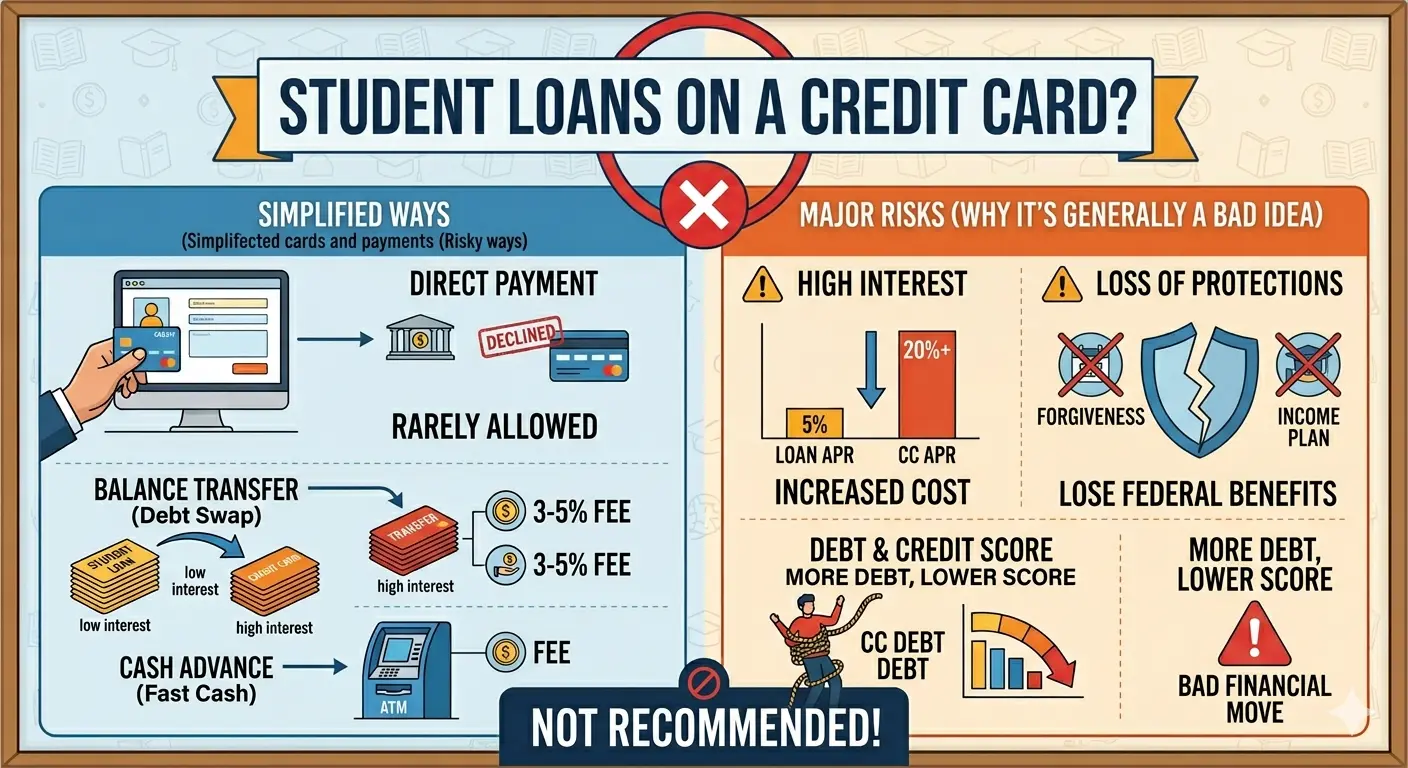

Why Direct Payments Face Immediate Rejection

If you log into your Nelnet, Mohela, or Aidvantage account right now, you will see options for ACH bank transfers and debit cards. However, you will notice a complete absence of a credit card payment option. The government explicitly prohibits this practice. The U.S. Department of Treasury enforces strict regulations preventing federal loan servicers from accepting revolving credit.

Moreover, the government implements this rule for your protection. Officials want to stop borrowers from shifting lower-interest student debt onto 25% APR credit cards. Such a shift often leads directly to bankruptcy. Similarly, private lenders like Discover and Sallie Mae block these transactions. Credit card companies charge merchants an interchange fee ranging from 1.5% to 3% per swipe. Private lenders already operate on thin margins. Therefore, they completely refuse to absorb these massive processing fees.

Creative Workarounds: How to Actually Make the Payment

Since direct portals reject your card, you must utilize indirect methods. If you remain determined to use your plastic, you have a few specific options available in 2026. However, you must execute these strategies carefully.

Method 1: Utilizing Third-Party Payment Processors

Third-party bill payment services provide the most common loophole. Platforms like Plastiq and Melio act as digital middlemen. First, you create an account on their platform. Next, you charge your student loan payment to your preferred credit card. Finally, the service cuts a physical check or issues an ACH transfer directly to your loan servicer.

The Major Drawback: These services survive by charging steep convenience fees. For instance, Plastiq currently charges a standard 2.9% fee per transaction. Consequently, this fee almost always wipes out the value of standard cash-back rewards.

Method 2: The Balance Transfer Strategy

Another powerful strategy involves balance transfers. Many credit card issuers mail promotional balance transfer checks to their customers. You can write one of these checks to your student loan servicer. This effectively transfers your loan balance onto your credit card.

This strategy makes sense only if you secure a 0% introductory APR offer. Furthermore, you must possess a solid plan to eliminate the debt before the promotional period ends. Otherwise, you will face standard interest rates that often exceed 20%.

You might feel tempted to take a cash advance from an ATM using your credit card to pay your loans. However, this is a terrible financial decision. Cash advances charge massive upfront fees. Moreover, they begin accruing exorbitant interest the very second the machine dispenses the cash. There is absolutely no grace period.

The Financial Math: Do the Rewards Justify the Fees?

Many borrowers chase airline miles and cash-back points. However, the mathematics rarely support this strategy. Let us examine the numbers closely to see why this approach often fails.

| Payment Strategy | Monthly Loan Amount | Processor Fee (2.9%) | Rewards Earned (2%) | Net Financial Result |

|---|---|---|---|---|

| Direct ACH (Bank Account) | $1,000 | $0.00 | $0.00 | Neutral ($0) |

| Using Plastiq with a 2% Card | $1,000 | $29.00 | $20.00 | Loss of $9.00 |

| Sign-Up Bonus Hack (Exception) | $3,000 | $87.00 | $500.00 (Bonus) | Gain of $413.00 |

As the table demonstrates, standard reward chasing results in a net loss. However, one specific exception exists. If you recently opened a new credit card and need to meet a high spending requirement (e.g., “Spend $3,000 in three months to earn $500”), paying your student loan via a third-party service can help you unlock that massive bonus. In this rare scenario, the sign-up bonus easily overshadows the transaction fee.

How Credit Card Payments Impact Your FICO Score

You must also consider your credit profile. Your credit utilization ratio determines 30% of your total FICO score. This ratio measures how much of your available credit you currently use.

Student loans classify as installment debt. Therefore, they do not affect your revolving credit utilization. However, if you dump a massive $5,000 student loan payment onto a credit card with a $10,000 limit, your utilization ratio instantly shoots up to 50%. Consequently, credit bureaus view you as a high-risk borrower. This action will severely damage your credit score. Furthermore, a lower score makes future borrowing much more expensive.

Smarter Alternatives to Avoid High-Interest Debt

If you struggle to afford your monthly payments, do not resort to credit cards. Instead, you should explore safer, government-backed alternatives.

- Apply for Income-Driven Repayment (IDR): For federal loans, you should apply for the SAVE plan or another IDR option immediately. The government recalculates your payment based entirely on your current income. Consequently, your payment could drop to $0 per month.

- Consider Student Loan Refinancing: If you possess strong credit and private loans, refinancing offers a great solution. You can secure a significantly lower interest rate. However, refinancing federal loans strips away all federal protections.

Frequently Asked Questions (FAQ)

No, you cannot. The U.S. Treasury Department strictly forbids federal loan servicers from accepting credit card payments. This regulation protects borrowers from converting low-interest educational debt into high-interest consumer debt.

Generally, it does not make sense. Plastiq charges a 2.9% transaction fee. Therefore, unless you are trying to reach a spending minimum for a massive credit card sign-up bonus, the high fees will easily cancel out your regular cash-back rewards.

You can use a balance transfer check from your credit card issuer to pay your loan servicer. This strategy works well if you secure a 0% introductory APR offer. However, you must pay an initial transfer fee of 3% to 5%.

Yes, it very likely will. Moving large loan amounts onto a revolving credit card drastically increases your credit utilization ratio. Consequently, lenders view you as a higher risk, which directly lowers your FICO score.