Does Your Credit Score Affect Student Loans? The Complete 2026 Guide

When planning for higher education, the last thing you want is an unexpected financial roadblock just before the semester begins. Many prospective college students and their parents constantly wonder: does your credit score affect student loans? The short and definitive answer is that it completely depends on the exact type of loan you are applying for. While some educational funding options ignore your financial past entirely, others scrutinize every single detail of your credit report. In this massive, comprehensive guide, we will break down exactly how your credit history interacts with your college funding, ensuring you make the smartest financial decisions for your future.

Key Takeaway: Federal loans for undergraduates usually do not require a credit check, but private student loans rely heavily on your credit score to determine approval and interest rates.

Understanding the Basics: How Credit Affects Student Loan Approvals

To successfully navigate the complex and often overwhelming world of college financing, you first need to understand that not all loans are created equal. The relationship between your creditworthiness and your borrowing power is a delicate balance determined largely by who is lending you the money. If you are asking whether a low credit score affects your student loan opportunities, we must divide the answer into federal funding and private funding.

Let’s explore these primary avenues of student funding and exactly how your three-digit credit file plays a role in each scenario.

Federal Student Loans: The Credit-Blind Educational Funding

For the vast majority of undergraduate students entering college, the federal government is the primary and most forgiving lender. The incredible advantage of federal funding is that, in most common cases, your credit score is completely irrelevant to the approval process. When you fill out the Free Application for Federal Student Aid (FAFSA), the U.S. Department of Education is evaluating your family’s financial need, not your personal credit history.

- Direct Subsidized Loans: Absolutely no credit check is required. These are strictly based on demonstrated financial need, and the government pays the interest while you are in school.

- Direct Unsubsidized Loans: Again, no credit check is required. These are available to undergraduate and graduate students regardless of financial need.

If you have a poor credit score, or simply no credit history at all (which is highly common for an 18-year-old recent high school graduate), these federal options are your safest, most accessible, and highly recommended first step.

The Federal Exception: Does Your Credit Affect PLUS Loans?

While standard undergraduate federal loans are highly lenient, the government does draw a strict line when it comes to Direct PLUS Loans. These specific loans are available to graduate or professional students, as well as the parents of dependent undergraduate students (often referred to as Parent PLUS Loans).

While the Department of Education does not demand a specific numerical “good” score (like a 700 or 750), they will conduct a mandatory credit check to look for an “adverse credit history.” If your credit report shows recent bankruptcies, foreclosures, tax liens, wage garnishments, or severe loan defaults, you might be denied a PLUS loan, regardless of what your actual FICO score is. Therefore, your credit history definitely impacts this specific federal student loan.

The Impact: Does Your Credit Score Affect Private Student Loans?

Now, let us shift our focus away from the government and look at the private sector. If you are applying for funding through a national bank, a local credit union, or an online financial institution (like Sallie Mae, Discover, or SoFi), the rules of the game change drastically. Does your credit score affect private student loans? Yes, absolutely, and it is the single most important factor in the application process.

Private lenders are taking on a massive financial risk by handing out thousands of dollars without collateral, and they use your credit profile as the primary metric to measure that risk.

Minimum Credit Requirements for Private Education Loans

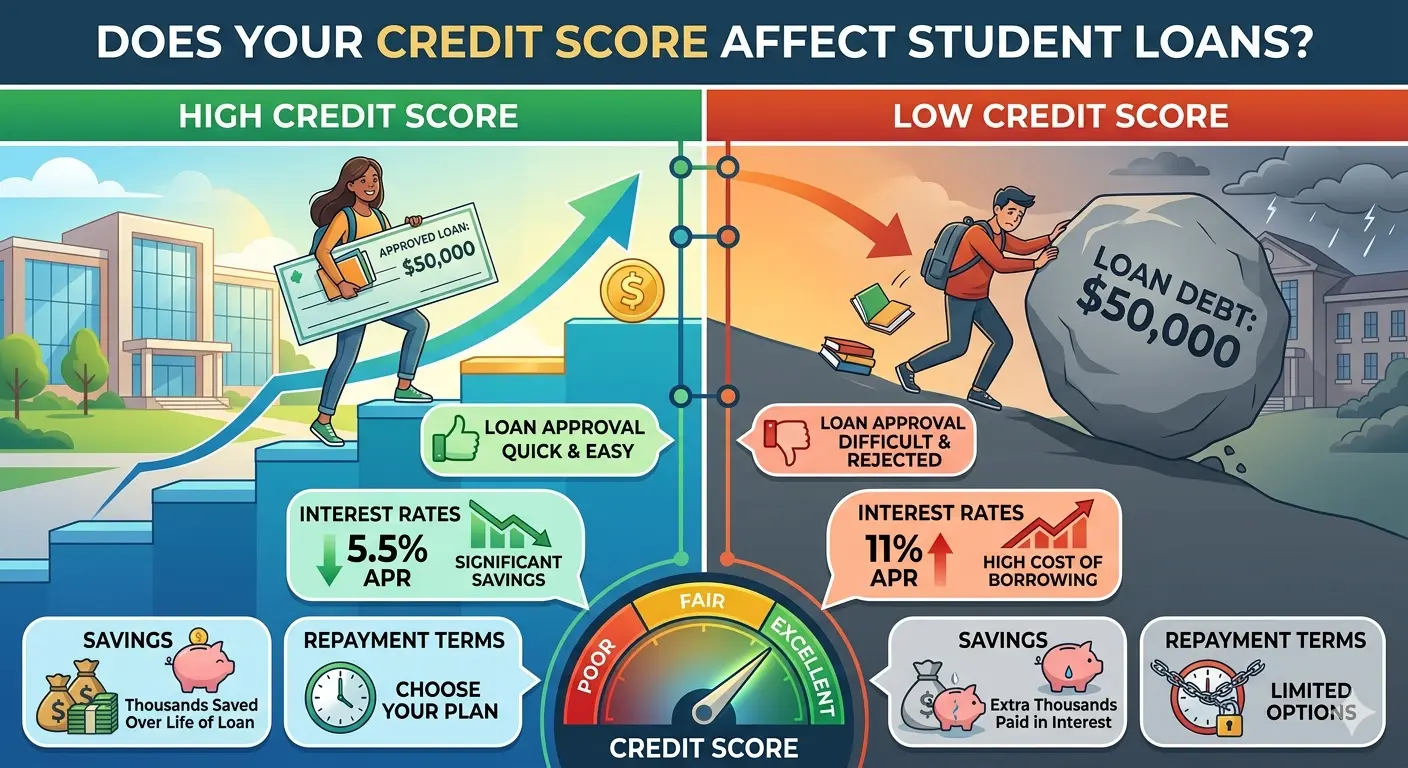

Unlike the federal government’s lenient approach, private educational lenders want to see a proven, lengthy track record of highly responsible financial behavior. Typically, to qualify for a private student loan purely on your own merit, you will need a credit score in the mid-to-high 600s at the bare minimum. A robust credit score in the 700s or above will significantly smooth out the application process and unlock much better terms.

Interest Rates and Your Credit Score

Your credit score doesn’t just dictate whether you get the green light for approval; it directly and heavily dictates how much that loan will ultimately cost you over the next 10 to 20 years. Private student loans offer variable or fixed interest rates, and the rate you are assigned is inextricably linked to your credit tier.

- Excellent Credit (750+): Secures the absolute lowest interest rates available on the market, potentially saving you tens of thousands of dollars over the lifetime of the loan.

- Good Credit (670-749): Usually results in standard approval with average, moderate interest rates.

- Poor Credit (Below 600): Will almost certainly result in a flat denial or exorbitant interest rates that make the loan unmanageable.

The Crucial Role of a Cosigner in Student Lending

Because most young college students lack the robust, lengthy credit history that banks desire, private lenders almost always require a cosigner. A cosigner is a trusted adult—usually a parent, guardian, or close relative—with strong credit who legally signs the loan document with you. By doing so, they agree to take full legal responsibility for paying back the debt if you default.

In a cosigned scenario, the private lender is primarily scrutinizing your cosigner’s credit score, not yours. If your credit score affects your student loan negatively, attaching a highly qualified cosigner instantly solves the problem and often lowers the interest rate dramatically.

Beyond Approval: How Education Loans Impact Your Future Credit

The intricate relationship between education debt and your financial profile is a continuous two-way street. Not only does your past credit dictate your immediate loan options, but your newly acquired student loans will instantly begin to shape and mold your future credit score.

Building Your Credit Mix and History

The very moment a student loan is fully disbursed to your university, it appears on your official credit report as an “installment loan.” For millions of young adults, this marks their very first major credit account. Interestingly, this actually improves your “credit mix” (having different types of diverse debt, such as revolving credit cards and fixed installment loans). It also starts the clock on your “length of credit history.” Both of these are highly positive ranking factors for your overall FICO score.

The Severe Danger of Late Student Loan Payments

The real financial test begins six months after graduation when the official repayment grace period ends. Student loan payments will soon account for a massive chunk of your overall “payment history,” which makes up a staggering 35% of your entire FICO score calculation.

Consistently making full, on-time payments month after month will slowly but steadily build a rock-solid, impressive credit profile. Conversely, missing payments, paying late, or allowing your loans to go into default will absolutely devastate your credit score. A ruined credit score will make it nearly impossible to buy a reliable car, rent a decent apartment, or secure a home mortgage for many years into the future.

Actionable Steps: Preparing Your Credit for Student Loans

If you are planning to apply for private student loans in the near future and are worried about how your credit score affects your student loan prospects, there are proactive steps you can take today to polish your financial profile.

- Check Your Credit Report: Pull your free annual credit report from all three major bureaus (Equifax, Experian, TransUnion). Dispute any fraudulent activities or errors immediately.

- Become an Authorized User: Ask a financially responsible parent to add you as an authorized user to an older, well-maintained credit card with a flawless payment history.

- Pay Down Existing Debt: If you already have credit cards, lower your credit utilization ratio by paying off as much of the balance as possible before applying for a student loan.

- Avoid Opening New Accounts: Each time you apply for new credit, a hard inquiry hits your report, which can temporarily ding your score. Avoid applying for store cards or auto loans right before seeking educational funding.

Conclusion: Navigating Credit and College Funding

So, does your credit score affect student loans? The answer remains a nuanced mix of federal leniency and strict private sector requirements. By maximizing your federal aid through the FAFSA first, you can bypass the stress of credit checks for the bulk of your educational expenses. However, if you find yourself needing private loans to bridge the gap, your credit score—or the score of a willing cosigner—becomes the master key to unlocking the funds you need for a brighter future.

Frequently Asked Questions

In most cases, no. Standard undergraduate federal funding, such as Direct Subsidized and Unsubsidized Loans, does not require a credit check. The application relies entirely on your FAFSA and financial need. However, Direct PLUS Loans for parents and graduate students do require a credit check to ensure there is no adverse credit history.

Yes, absolutely. Private lenders heavily scrutinize your credit report to determine whether you qualify for educational funding. Your credit score directly impacts your approval odds and determines the interest rate you will receive on the private student loan.

It is exceptionally difficult to get approved for private funding with poor credit or an unestablished credit history on your own. Most college students solve this issue by applying with a creditworthy cosigner, which allows the lender to base the approval and interest rates on the cosigner’s excellent credit score.

Initially, applying for a private loan may cause a small, temporary dip in your score due to the hard inquiry. However, in the long run, having an installment loan improves your credit mix and establishes your credit history. Making consistent, on-time payments after graduation will significantly boost your overall credit score.