If you have been paying off a second mortgage and keeping an eye on the ever-changing real estate market, you might have found yourself wondering: can you refinance a home equity loan? The short and simple answer is yes. Just as you can refinance your primary mortgage to take advantage of better interest rates or to change your repayment terms, you can absolutely refinance a home equity loan. In fact, doing so at the right time could save you thousands of dollars, lower your monthly obligations, or give you access to even more cash for major life expenses.

However, refinancing is not a one-size-fits-all solution. It involves a new application process, potential closing costs, and a careful evaluation of your current financial standing. In this comprehensive guide, we will explore everything you need to know about refinancing your home equity loan. We will cover the profound benefits, the potential drawbacks, real-life financial scenarios, the exact steps to qualify, and alternative options you might not have considered.

Understanding Home Equity Loan Refinancing

Before diving into the mechanics of the process, it is essential to understand what refinancing a home equity loan actually entails.

A home equity loan, frequently referred to as a second mortgage, allows you to borrow a lump sum of money against the equity you have built up in your property. You then repay this amount over a fixed term with a fixed interest rate.

When you refinance this loan, you are essentially applying for a brand-new loan to pay off the existing one. The new loan will come with its own set of terms, an updated interest rate, and a new repayment schedule. Because your financial situation and the broader economic landscape have likely changed since you took out the original loan, this new agreement can be tailored to better suit your current needs.

6 Major Reasons to Refinance Your Home Equity Loan

Why go through the paperwork and hassle of applying for a new loan? Homeowners typically choose to refinance their equity loans to achieve one or more of the following financial goals:

1. Securing a Lower Interest Rate

This is the primary motivation for most borrowers. If the national interest rates have dropped since you originated your original loan, or if your personal credit score has significantly improved, you may qualify for a much lower rate. Lowering your rate by even 1% or 2% can lead to massive savings over the life of the loan.

2. Lowering Your Monthly Payment

If your household budget has tightened due to career changes, medical expenses, or inflation, lowering your monthly debt obligation can provide immediate relief. You can achieve a lower monthly payment either by securing that lower interest rate or by extending the repayment term of your new loan.

3. Transitioning from an Adjustable Rate to a Fixed Rate

While most home equity loans have fixed rates, some homeowners originally opted for a Home Equity Line of Credit (HELOC), which usually carries a variable interest rate. If market rates are rising, your monthly payments on a HELOC can skyrocket. Refinancing your HELOC into a fixed-rate home equity loan provides long-term stability and protects you from future rate hikes.

4. Borrowing Additional Funds (Cash-Out)

If the market value of your property has increased, your total home equity has grown along with it. By refinancing your current home equity loan, you can take out a larger loan amount. The new loan pays off the old balance, and you receive the remaining difference in a lump sum. This cash can be used for home renovations, consolidating high-interest credit card debt, or covering university tuition fees.

5. Shortening the Loan Term

Conversely, if your financial situation has vastly improved, you might want to get out of debt faster. By refinancing into a shorter-term loan (for example, moving from a 15-year term to a 5-year term), your monthly payments will increase, but you will save a tremendous amount of money in total interest payments and own your home free and clear much sooner.

6. Debt Consolidation

Many homeowners use the opportunity of a refinance to consolidate other debts. If you have accrued high-interest personal loans or credit card balances, rolling those debts into a new, lower-interest home equity loan can streamline your finances into one single, manageable monthly payment.

The Drawbacks and Risks: What Lenders Might Not Tell You

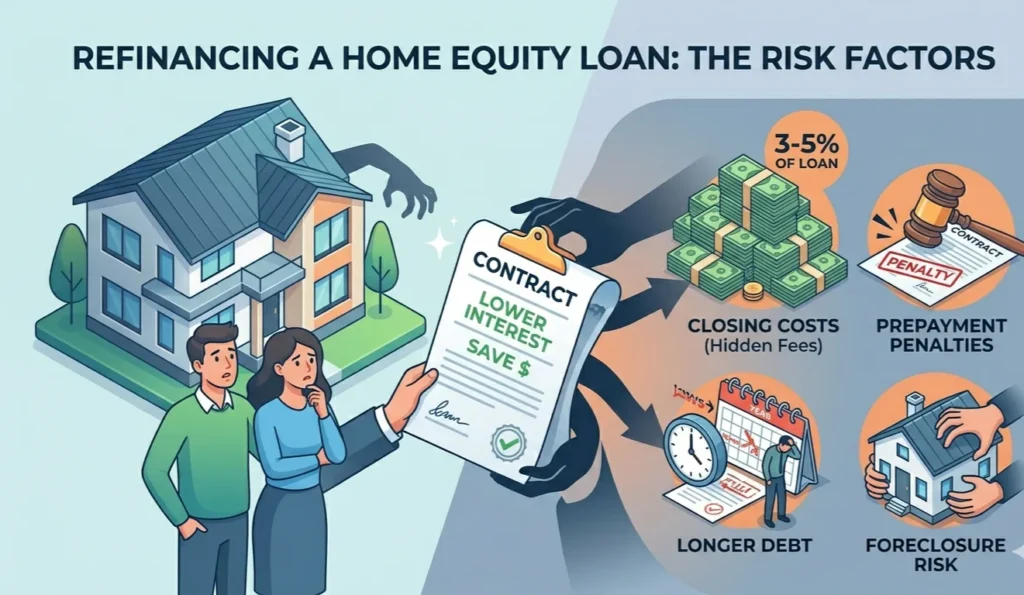

While the benefits are highly attractive, refinancing is not without its pitfalls. It is crucial to weigh these potential drawbacks before signing any new paperwork.

Closing Costs and Fees

Refinancing a second mortgage is not free. Just like your original mortgage, a new home equity loan comes with closing costs. These typically range from 2% to 5% of the total loan amount. Costs can include application fees, appraisal fees, title search fees, and origination fees. You must calculate your “break-even point”—the number of months it will take for your monthly savings to surpass the upfront costs of refinancing.

Prepayment Penalties

Check the fine print on your existing home equity loan. Some lenders include a prepayment penalty clause, meaning they will charge you a hefty fee if you pay off the loan early (which is exactly what happens when you refinance). This fee could easily negate the savings you hoped to achieve.

Risking Your Home

Remember that your house serves as the collateral for this loan. If you refinance to take out more cash or agree to higher monthly payments for a shorter term, and you suddenly lose your income, you risk foreclosure.

Extending the Life of Your Debt

If you refinance a loan that you have already been paying down for five years into a new 15-year loan, you are resetting the clock. While your monthly payment will drop, you will be in debt for a much longer period and will likely pay far more in total interest over the lifespan of the loan.

Real-Life Case Studies: Does Refinancing Make Sense?

To make these concepts more concrete, let’s look at two practical scenarios where refinancing does and doesn’t make sense.

Case Study 1: The Smart Refinance (The Break-Even Win)

Sarah took out a $50,000 home equity loan three years ago at an 8.5% interest rate for a 15-year term. Her credit score was average at the time. Today, her credit score has jumped to 780, and market rates have dropped. She qualifies for a new rate of 5.5%.

If she refinances the remaining balance, her monthly payment drops significantly. Even with $1,500 in closing costs, the monthly savings mean she will break even in just 14 months. Since she plans to stay in the home for another ten years, this refinance is a brilliant financial move.

Case Study 2: The Costly Mistake (The Equity Trap)

Mark has a $30,000 home equity loan at 6.5%. He wants to lower his monthly payment because his budget is tight, so he looks into refinancing to a new 15-year term at 6.0%. However, Mark’s original loan only has 5 years left. By refinancing, he lowers his monthly payment by a small margin, but he resets his debt clock to 15 years. Furthermore, his current lender charges a $500 prepayment penalty, and the new closing costs are $1,200. Over the new 15-year term, Mark will end up paying thousands of dollars more in interest just to save a few bucks a month right now.

Step-by-Step Guide: How to Refinance a Home Equity Loan

If you have crunched the numbers and decided that refinancing is the right path for you, here is the exact process you need to follow.

Step 1: Calculate Your Current Equity

Lenders will not approve a refinance if you do not have enough equity in your home. To estimate your equity, take the current market value of your home and subtract the balance of your primary mortgage AND the balance of your current home equity loan.

(Example: Your home is worth $400,000. You owe $200,000 on your primary mortgage and $30,000 on your home equity loan. Your total debt is $230,000. You have $170,000 in equity).

Step 2: Check Your Credit Score and Credit Report

Your credit score dictates the interest rate you will be offered. Pull your credit report from all major credit bureaus. Ensure there are no fraudulent accounts or errors dragging your score down. A score of 680 or higher is generally required, but a score of 740 or above will unlock the best premium rates.

Step 3: Calculate Your Debt-to-Income (DTI) Ratio

Lenders want to ensure you are not over-leveraged. Your DTI ratio represents the percentage of your gross monthly income that goes toward paying debts. Ideally, your total monthly debt payments (including the new loan, credit cards, auto loans, etc.) should not exceed 43% of your gross monthly income.

Step 4: Shop Around and Compare Offers

Do not just blindly accept an offer from your current lender. Request quotes from at least three different financial institutions, including massive national banks, local credit unions, and online-only lenders. Compare the Annual Percentage Rate (APR), which includes both the interest rate and the fees, to get a true picture of the loan’s cost.

Step 5: Gather Documentation and Apply

Once you select a lender, you will need to submit a formal application. Be prepared to provide extensive documentation, including:

- Recent pay stubs (usually the last 30 days)

- W-2 forms or 1099s from the past two years

- Federal tax returns from the past two years

- Recent bank statements

- Proof of homeowners insurance

- Your most recent primary mortgage statement

Step 6: The Home Appraisal

In most cases, the new lender will require a fresh appraisal of your property to confirm its current market value. This ensures they are not lending you more money than the home is actually worth.

Step 7: Closing and Funding

If the underwriting team approves your application, you will move to closing. You will sign the new loan documents and pay any out-of-pocket closing costs (unless they have been rolled into the new loan balance). The lender will then use the funds from the new loan to pay off your old home equity loan entirely.

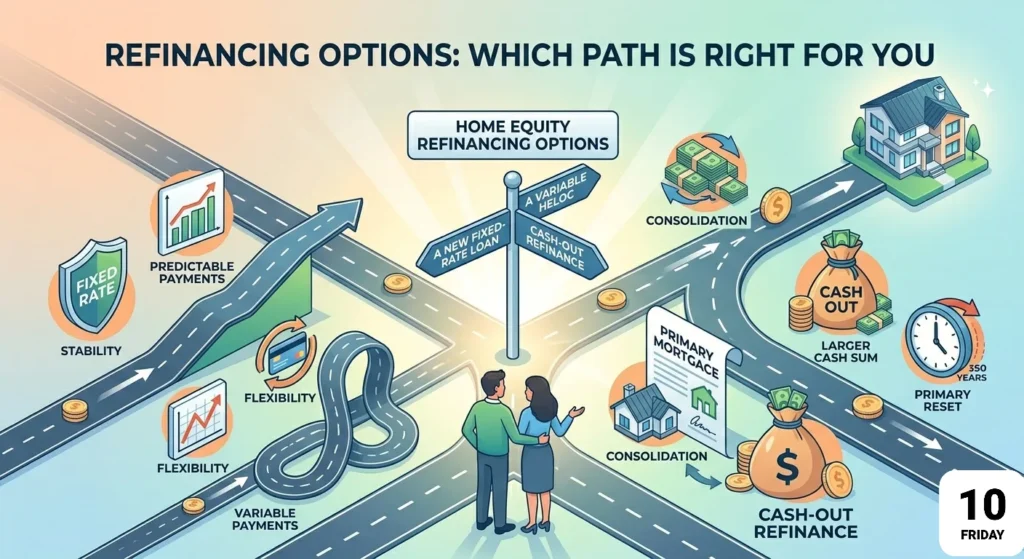

Refinancing Options: Which Path is Right for You?

When replacing your current equity loan, you have three distinct pathways. Choosing the right one depends entirely on your long-term financial strategy.

1. A New Home Equity Loan

This is a straightforward swap. You replace your old home equity loan with a new one. You retain the stability of a fixed interest rate and a predictable monthly payment. This is ideal if you simply want a better rate or need to adjust your repayment term without changing how your debt functions.

2. A Home Equity Line of Credit (HELOC)

You can choose to refinance your lump-sum loan into a revolving line of credit. A HELOC acts much like a high-limit credit card tied to your home’s equity. You are approved for a maximum limit, but you only borrow what you need, when you need it, and you only pay interest on the amount you actively use.

Pros: Incredible flexibility; lower initial payments (often interest-only during the draw period).

Cons: Variable interest rates mean your payments can suddenly spike if market rates increase.

3. A Cash-Out Refinance

A cash-out refinance is a much larger maneuver. Instead of just replacing your second mortgage, a cash-out refinance replaces your primary mortgage and your home equity loan with one giant, unified loan.

Pros: You consolidate all housing debt into a single payment, often at a lower interest rate than second mortgages offer.

Cons: You reset the term on your entire house payoff. Closing costs for a primary mortgage refinance are significantly higher than for a home equity loan.

What If You Have Bad Credit?

If your credit score has taken a hit since you secured your original loan, refinancing becomes substantially more challenging, but not impossible.

- Seek Out Credit Unions: Local credit unions often have more flexible underwriting criteria than massive corporate banks and may be willing to look at your entire financial picture rather than just a threedigit score.

- Bring a Co-Signer: Having a spouse or family member with excellent credit co-sign the new loan can mitigate the lender’s risk.

- Focus on LTV: If your Loan-to-Value (LTV) ratio is exceptionally low (meaning you own a vast majority of your home’s value outright), lenders may overlook a poor credit score because their investment is heavily protected by the physical asset.

Powerful Alternatives to Refinancing

If the closing costs are too high, or if you simply cannot qualify for a better rate right now, there are alternative avenues to explore.

1. Loan Modification

If your primary goal for refinancing is that you are struggling to make your monthly payments, contact your current lender immediately. Do not wait until you miss a payment. Many lenders offer “loan modification” programs for borrowers experiencing financial hardship. They may temporarily lower your interest rate, extend your term, or pause payments without requiring a full refinance application or charging closing costs.

2. Personal Unsecured Loans

If you need additional cash but do not want to use your home as collateral again, consider a personal loan. While interest rates on personal loans are generally higher than home equity products, they fund much faster (often within 24-48 hours) and require absolutely no closing costs or home appraisals.

3. 0% APR Balance Transfer Credit Cards

If your goal was to do a cash-out refinance to pay off $10,000 in credit card debt, look into balance transfer cards instead. Many credit card companies offer introductory 0% APR periods for 12 to 21 months. If you can aggressively pay off the debt within that window, you will save thousands in interest and avoid touching your home’s equity altogether.

Frequently Asked Questions

Absolutely. In fact, starting with your current lender is a great idea. They already have your property information and payment history on file. They may even offer loyalty discounts or waive certain application fees to keep your business. However, you should still shop around to ensure their offer is actually competitive.

Legally, there is often no strict waiting period, meaning you could theoretically refinance a few months after taking out the original loan. However, practically speaking, you should wait until you have built up more equity, or until market rates have dropped enough to justify the closing costs.

The rules regarding tax deductions for home equity loans have changed in recent years. Generally, the interest on a home equity loan is only tax-deductible if the funds are used to “buy, build, or substantially improve” the home that secures the loan. Closing costs themselves are rarely entirely deductible in the year you close; they usually must be amortized over the life of the loan. Always consult a licensed CPA or tax advisor for your specific situation.

When you apply for a refinance, the lender will perform a “hard inquiry” on your credit report. This typically drops your score by a few points temporarily. Additionally, closing your old loan account and opening a new one alters the average age of your credit history, which can cause a slight, short-term dip. However, if refinancing helps you make your payments on time and lowers your credit utilization, your score will ultimately improve in the long run.

Final Thoughts: Making the Right Move for Your Future

So, can you refinance a home equity loan? Yes. Should you? That depends entirely on the math.

Refinancing a second mortgage is a powerful financial tool that can help you adapt to changing economic climates and personal milestones. Whether you are hunting for a significantly lower interest rate, aiming to transition into the flexibility of a HELOC, or looking to cash out equity to build your dream home addition, the options are plentiful.

The secret to a successful refinance lies in preparation. Do not rush the process. Calculate your break-even point with ruthless precision. Audit your credit report, compare Loan Estimates from multiple reputable lenders, and thoroughly read the fine print regarding prepayment penalties and hidden fees. By treating your home equity as the valuable, hard-earned asset that it is, you can ensure that your refinancing journey leads directly to greater financial freedom and long-term stability.