When the grace period ends and that first massive student loan bill arrives, a chill can easily run down your spine. For millions of graduates worldwide, the crushing weight of educational debt isn’t just a financial burden; it is a psychological hurdle. So, a very raw, terrifying question often bubbles up in the dead of night: What happens if you don’t pay your student loans? Is it just a matter of getting a few annoying phone calls, or are we talking about ruined credit, seized tax refunds, and garnished wages?

The short answer: Ignoring your student debt is one of the most dangerous financial decisions you can make. The consequences are severe, far-reaching, and heavily dependent on whether your loans are federal or private. However, panicking won’t solve the issue. Action will.

In this comprehensive guide, we will break down exactly what happens when you miss a payment, the critical differences between delinquency and default, and most importantly, the actionable steps you can take today to protect your financial future.

Understanding the Timeline: From Missed Payment to Default

To grasp the full impact of unpaid student loans, you must first understand the timeline. Financial institutions do not immediately seize your assets the day after a missed payment. There is a specific, legally defined progression from the moment you are late to the moment you are officially in default.

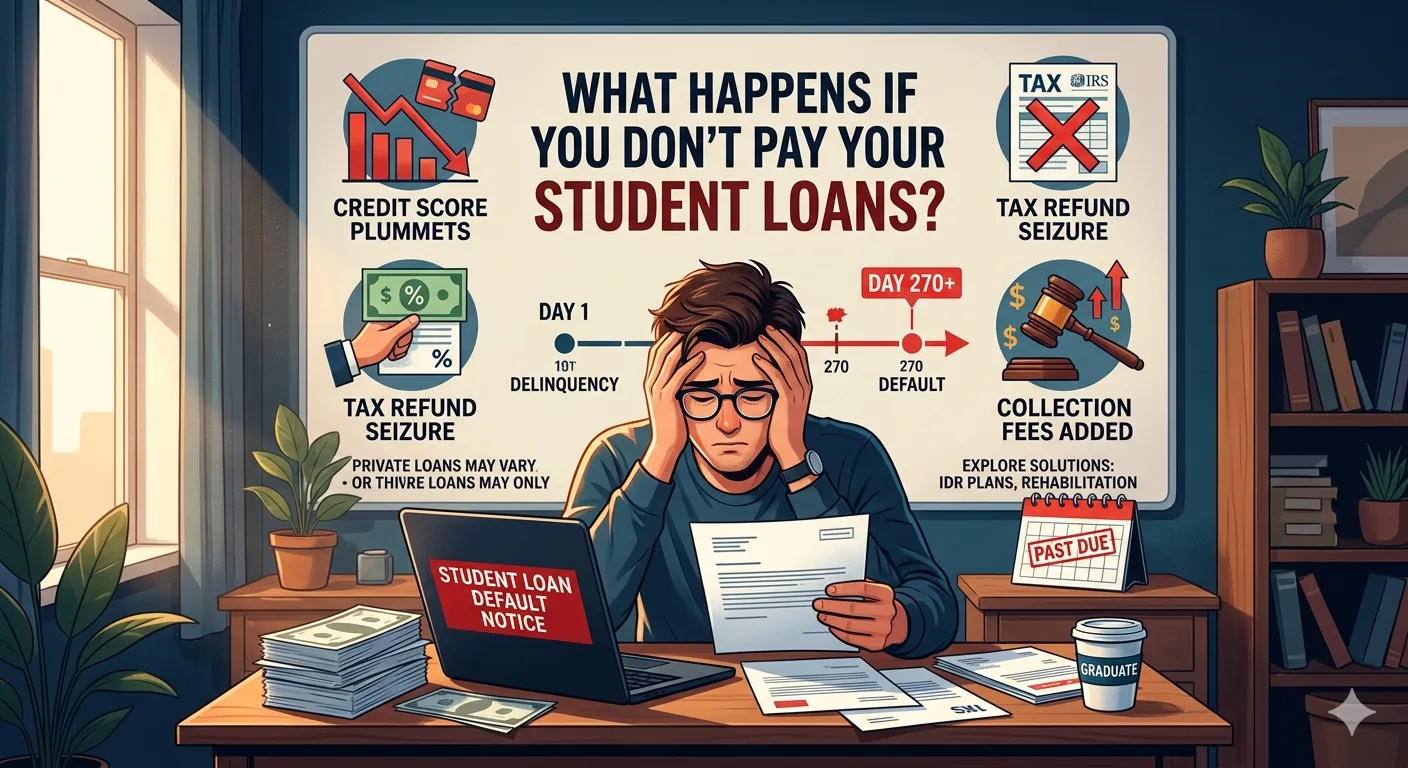

Phase 1: Delinquency (Day 1 to Day 269)

The very first day after you miss a payment, your loan becomes delinquent.

Let’s say your payment was due on the 1st of the month. On the 2nd, you are delinquent. Initially, the consequences are mild but annoying. Your loan servicer will begin attempting to contact you. You will receive emails, letters, and phone calls.

The 90-Day Mark: The Credit Score Impact

While your loan is delinquent from day one, the real damage begins at the 90-day mark. If you fail to make a payment for 90 consecutive days, your loan servicer will officially report the delinquency to the three major national credit bureaus (Equifax, Experian, and TransUnion).

What does this mean for you?

- Credit Score Plummet: Your credit score will take a significant hit. A lower credit score affects your ability to rent an apartment, buy a car, secure a mortgage, or even get a cell phone plan.

- Future Borrowing is Compromised: Other lenders will see you as a high-risk borrower. If you are approved for future credit, it will come with exorbitant interest rates.

Phase 2: The Danger Zone (Day 270+)

If you continue to ignore the communications and remain delinquent for 270 days (roughly nine months), the situation escalates dramatically. For federal student loans, day 270 marks the official transition from delinquency to default.

Note: For private student loans, default can happen much faster—often after just 90 to 120 days of missed payments, depending on your specific lender’s terms.

The Devastating Consequences of Student Loan Default

Defaulting on a student loan triggers a cascade of aggressive collection tactics. The government (and private lenders) have immense power to recoup their money. If you have been wondering what happens if you don’t pay your student loans, this is where the reality gets harsh.

1. Acceleration of the Entire Loan Balance

The moment you default, the concept of “monthly payments” vanishes. The entire unpaid balance of your loan—plus any accumulated interest—becomes immediately due and payable. This is known as “acceleration.” You lose access to all standard repayment plans, deferment options, and forbearance.

2. Wage Garnishment

This is perhaps the most frightening consequence for working professionals. If you default on federal student loans, the government does not need a court order to take your money. They can mandate that your employer withhold up to 15% of your disposable pay and send it directly to the government to cover your debt.

Private lenders can also garnish your wages, but they must successfully sue you in court first. Once they have a judgment against you, they can tap directly into your paycheck.

3. Treasury Offset (Tax Refund Seizure)

Were you looking forward to your annual tax refund to pay for a vacation or cover essential bills? If you are in default on a federal student loan, the government will intercept your federal and, in some cases, state tax refunds. This process, known as the Treasury Offset Program, applies your refund directly to your defaulted loan balance. They can also withhold other federal payments, including parts of your Social Security benefits.

4. Loss of Professional Licenses

In some jurisdictions, the consequences extend beyond pure finance and bleed directly into your career. Several states have laws that allow them to suspend or revoke professional licenses (such as nursing, teaching, or law licenses) if the holder defaults on their student loans. You could quite literally lose your ability to work in your chosen profession.

5. Ballooning Debt due to Collection Fees

When your loan goes into default, it is typically transferred to a third-party collection agency. These agencies charge exorbitant collection fees, which can legally be upa to 18.5% of your outstanding principal and interest. These fees are added to your total balance, making it even harder to dig yourself out of the hole.

Federal vs. Private Student Loans: Different Rules of Engagement

It is crucial to distinguish between federal and private loans because the consequences of non-payment vary significantly.

Federal Student Loans

Backed by the government, federal loans offer more leeway initially but possess terrifying collection powers once in default.

- Default Timeline: Usually 270 days.

- Collection Powers: No court order needed for wage garnishment or tax refund seizure.

- Forgiveness Options: Highly structured relief programs exist (Income-Driven Repayment, Public Service Loan Forgiveness).

Private Student Loans

Issued by banks, credit unions, or private entities (like Sallie Mae or SoFi).

- Default Timeline: Varies by contract, often 90-120 days.

- Collection Powers: Must sue you in court to garnish wages or seize assets. They cannot intercept your tax refund.

- Statute of Limitations: Unlike federal loans, private student loans have a statute of limitations (usually 3 to 10 years, depending on your state). If the lender doesn’t sue you within this timeframe, they lose the legal right to force repayment through the courts.

How to Avoid Default: Proactive Solutions

Now that we have explored the dark side of what happens if you don’t pay your student loans, let’s pivot to the light. If you are struggling, do not bury your head in the sand. You have multiple safety nets available.

Solution 1: Income-Driven Repayment (IDR) Plans

If your income drops or you lose your job entirely, immediately apply for an Income-Driven Repayment plan (for federal loans). These plans cap your monthly payment at a percentage of your discretionary income. If you are unemployed or earning very little, your legally required monthly payment could drop to exactly $0.

Yes, a $0 payment counts as an “on-time payment” and keeps your loan in good standing.

Solution 2: Deferment and Forbearance

If you are facing a temporary hardship—like a medical emergency, a transition between jobs, or a return to school—you can apply for deferment or forbearance. These programs temporarily pause your requirement to make monthly payments.

- Deferment: In some cases, the government will pay the interest that accrues on subsidized loans during a deferment.

- Forbearance: Interest will continue to accrue on all loan types, but you get a temporary break from the cash-flow drain.

Solution 3: Direct Consolidation

If your loans are already in default, you might be able to drag them out of the mud through Direct Loan Consolidation. By combining your defaulted federal loans into a new Direct Consolidation Loan, you effectively pay off the old loans and start fresh. To qualify, you must typically agree to repay the new loan under an Income-Driven Repayment plan.

Solution 4: Loan Rehabilitation

Loan rehabilitation is a powerful program for federal loans. You must agree in writing to make nine voluntary, reasonable, and affordable monthly payments within a 10-month period. Your loan servicer will determine this payment amount based on your income (it can be as low as $5 a month). Once you complete the rehabilitation, the default status is entirely erased from your credit history.

Solution 5: Negotiating with Private Lenders

If you have private loans, your options are different but not nonexistent. Call your lender before you miss a payment. Many private lenders offer their own version of short-term forbearance or hardship programs. They want to avoid the legal fees of suing you, so they are often willing to temporarily lower your interest rate or accept interest-only payments for a few months until you get back on your feet.

The Myth of Bankruptcy and Student Loans

There is a persistent myth that student loans can never be discharged in bankruptcy. While it is incredibly difficult, it is not legally impossible.

To discharge student loans in bankruptcy, you must file a separate action known as an “adversary proceeding” and prove to the court that repaying the loan would impose an “undue hardship” on you and your dependents. Courts typically use the Brunner Test to determine this, which requires you to prove:

- You cannot maintain a minimal standard of living if forced to repay the loans.

- Your financial situation is likely to persist for a significant portion of the repayment period.

- You have made good faith efforts to repay the loans before filing for bankruptcy.

It is a grueling legal battle, but recent policy changes at the Department of Justice have aimed to make the bankruptcy discharge process slightly more accessible for severely distressed borrowers.

Frequently Asked Questions

Can I go to jail for not paying my student loans?

Does student debt eventually just go away if ignored?

What happens to my cosigner if I don’t pay?

Can the government seize my tax refund for unpaid student loans?

Final Thoughts: Taking Back Control

The thought of not being able to afford your debt is paralyzing. The anxiety associated with the keyword what happens if you don’t pay your student loans is entirely valid. The consequences are designed to be punitive.

However, knowledge is the ultimate antidote to financial fear. Whether it is switching to an Income-Driven Repayment plan, entering a rehabilitation program, or aggressively restructuring your personal budget, the power lies in proactive communication. Do not ignore the letters. Do not ghost your loan servicer. Reach out, explain your situation, and utilize the legal frameworks designed to help struggling borrowers. Your financial future depends on taking that first, brave step of facing the numbers head-on.